IRS Notices

Why Did I Get a Letter From the IRS? What It Means and What to Do (2026)

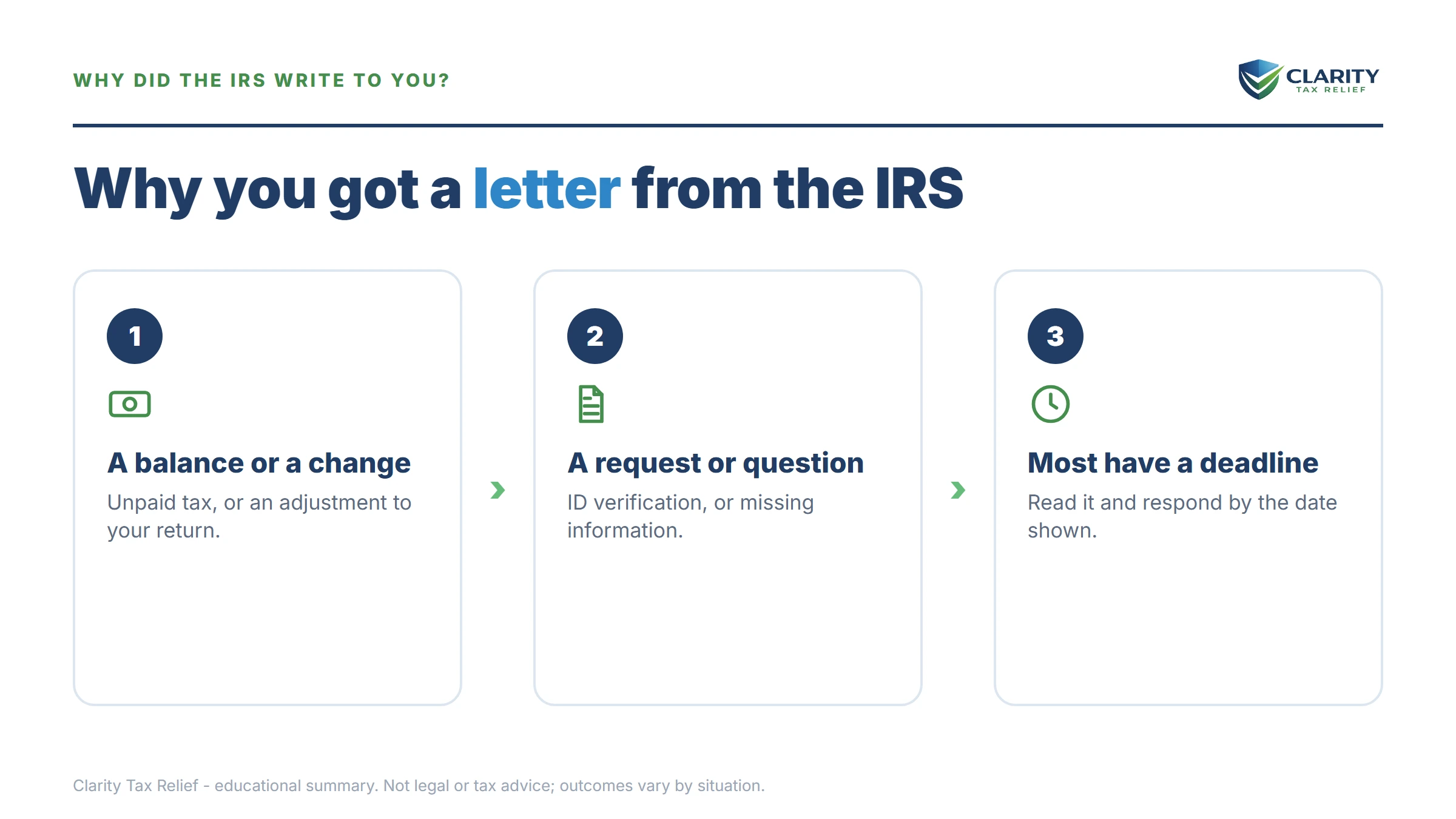

The short answer: if you're asking "why did I get a letter from the IRS," it's almost always because something on your tax account needs attention — a balance due, a math correction, a question about your return, a changed refund, or an identity check. The notice number in the top corner tells you exactly which one. Most are routine and fixable.

⏱ Your deadline: nearly every IRS letter prints a response or "pay by" date — often 21 to 30 days from the notice date. That date matters. After it passes, the IRS's automated system moves to the next step on its own. Open the letter and find that date today.

Why the IRS sent you a letter

Take a breath. A letter from the IRS is not a knock at the door, and it rarely means you're in trouble. The IRS contacts taxpayers almost entirely by mail, and it sends millions of letters every year for ordinary reasons. The question isn't whether to worry — it's which letter you got, because the code in the corner tells you everything.

Here are the most common reasons a letter from the IRS lands in your mailbox:

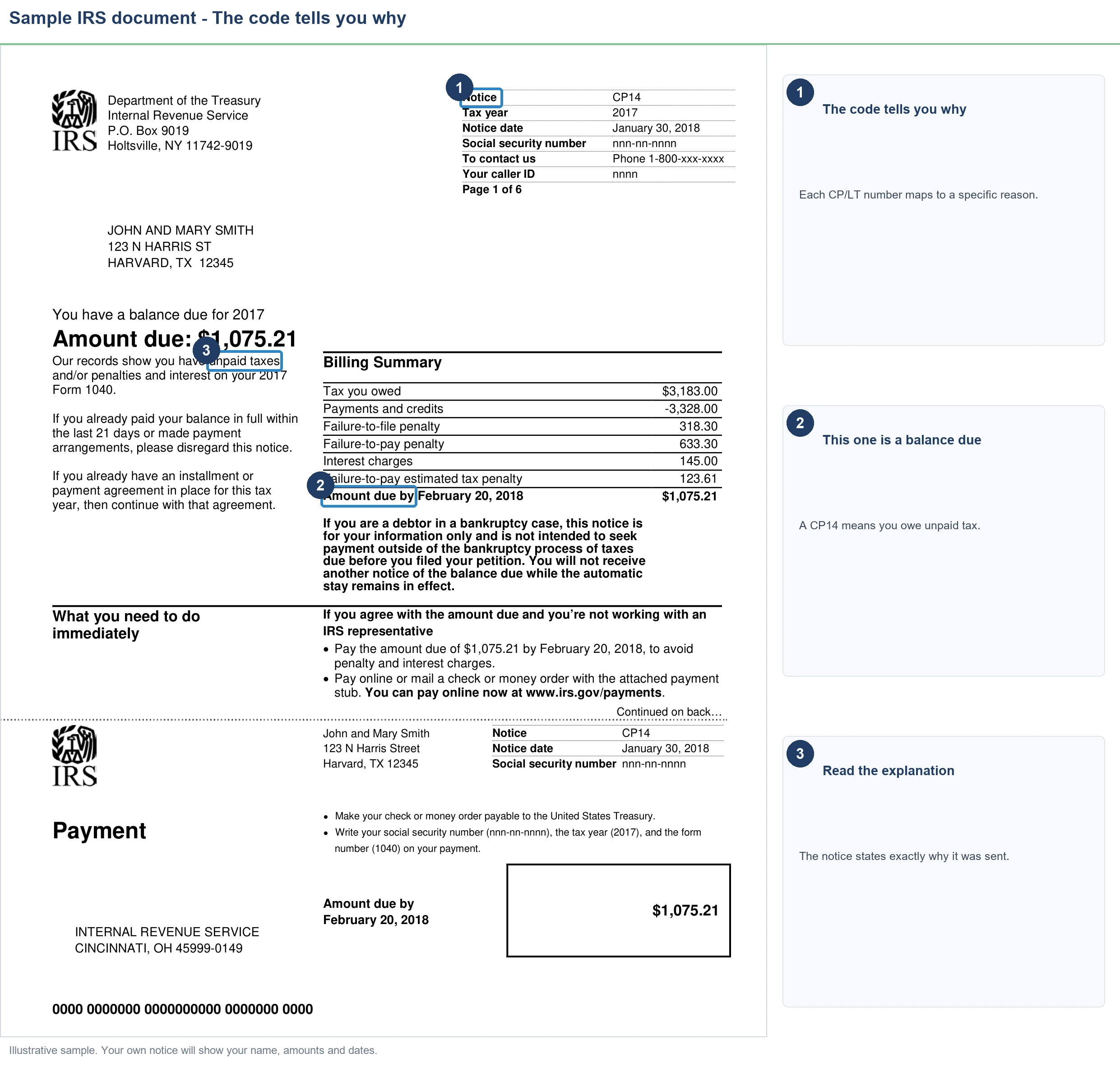

- You owe a balance. The most common letter, a CP14, is the first bill for unpaid tax. If that's what you're holding, read our full CP14 notice guide.

- The IRS changed your return. A math error, a missing form, or income that didn't match what an employer reported can trigger a correction notice (like a CP2000), which adjusts what you owe or your refund.

- Your refund changed. Some letters explain why your refund was larger, smaller, or held — often because of an offset for another debt.

- The IRS needs to verify your identity. Letters like 5071C or 4883C ask you to confirm it's really you before your return finishes processing.

- A return is missing. If the IRS expected a filing it didn't receive, it asks for it.

The IRS keeps a plain-language directory of these at Understanding your IRS notice or letter. Find your number and you'll find the official explanation.

How to read your IRS letter in two minutes

Before you do anything else, find these four things on the page:

- The notice or letter number — top or bottom right corner. It starts with CP (a computer-generated notice) or LTR/Letter followed by digits. This is the single most important detail.

- The tax year it refers to. Make sure it matches a return you actually filed.

- The amount, if any — and whether it breaks down into tax, penalties, and interest.

- The response or pay-by date — your real deadline.

Once you have the notice number, you can look it up on IRS.gov and know in plain English what the letter wants and what your options are.

What happens if you ignore a letter from the IRS

This is where delay costs the most. The IRS notice system is automated. If your letter is a balance-due notice and you don't respond, the next letter is already queued — and each one carries more weight than the last:

- CP14 — first bill. No enforcement yet. This is the cheapest moment to act.

- CP501 / CP503 — reminder notices. Still just bills, but penalties and interest keep climbing.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a real risk.

- LT11 / Letter 1058 — Final Notice, usually sent by certified mail. After 30 days the IRS can garnish wages and levy bank accounts. You have formal appeal rights here — but far fewer good options than you had at the first letter.

Identity-verification and missing-return letters work differently, but ignoring those is just as costly: your refund stays frozen, or the IRS files a return for you that leaves out every deduction you'd qualify for. Either way, the system doesn't forget. Responding — even just to ask for time — stops the automatic next step.

Make sure the letter is real (and right)

Scammers impersonate the IRS constantly, so confirm before you pay or share anything:

- Real IRS letters come by postal mail. The IRS does not start contact by email, text, or social media. If you got a "letter" any other way, it's a scam.

- Payment goes only to the United States Treasury or through IRS.gov. Gift cards, wire transfers, and payment apps are red flags every time.

- Verify the balance yourself. Log into your IRS online account and compare it to the letter. Notices and recent payments often cross in the mail, and some notices are simply wrong.

Got a certified letter from the IRS? Don't let it sit unopened out of fear — certified mail usually marks a deadline that protects your legal rights, which means it's the most important kind to open the same day.

Not sure what your IRS letter means?

Send us a photo of it. An experienced tax professional will tell you exactly which notice you have, what your deadline is, and what your options are — free, confidential, and no pressure.

How to respond, step by step

- Find the notice number and deadline. Look them up at the IRS notice directory so you know exactly what it is.

- Verify it against your records. Check your IRS online account and the return for that year. Confirm the amount, the tax year, and any payments you already made.

- If it's correct and asks for money you can pay: pay by the deadline at IRS.gov/payments. That stops penalties and the notice sequence right away.

- If it's correct but you can't pay in full: you have options the letter doesn't advertise — a short-term plan (up to 180 days), a monthly installment agreement (streamlined for balances under $50,000, up to 72 months), hardship status that pauses collection, or penalty relief if this is your first slip in years.

- If the letter is wrong or you already paid: respond in writing with proof, and keep copies of everything. Don't pay a balance twice on the assumption the IRS will catch its own error.

- If it's a verification letter: follow its instructions exactly — usually a phone call or an online ID check — so your return can finish processing.

- If you owe more than $10,000, have unfiled years, or just want it handled: get a professional review first. The order you fix things in — returns, then penalties, then the balance — changes what you end up paying.

If a deadline already passed or you can't reach the IRS, the independent Taxpayer Advocate Service can help when the normal channels break down.

Common IRS letter questions, answered

Why did I get a letter from the IRS?

The IRS mails a letter when something on your account needs attention — a balance due, a math correction, a question about your return, a refund change, or an identity check before processing. The notice or letter number in the top corner tells you exactly which one it is. Most are routine and fixable.

Where is the notice number on an IRS letter?

Look in the top or bottom right corner. It starts with CP (a computer-generated notice, like CP14 or CP2000) or LTR/Letter followed by numbers (like LT11 or Letter 4883C). That code identifies exactly what the letter is and what it wants — search it on IRS.gov to read the official explanation.

Does a letter from the IRS mean I'm being audited?

Usually no. Most IRS letters are bills, reminders, or requests to verify information — not audits. A true audit arrives as a specific examination letter. Even then, many audits are handled entirely by mail. Read your notice number before assuming the worst, because the code tells you what's actually happening.

How do I know if an IRS letter is real or a scam?

A real IRS letter arrives by postal mail — never by email, text, or social media. It has a notice or letter number, references a specific tax year, and directs payment only to the United States Treasury or through IRS.gov. Anyone demanding gift cards, wire transfers, or payment apps is a scammer.

What happens if I ignore a letter from the IRS?

It depends on the letter, but ignoring it almost always makes things worse. Balance-due notices escalate on an automated schedule toward liens, levies, and wage garnishment. Verification requests can freeze your refund. Responding — even just to ask for time — stops the automatic next step.

Why did I get a certified letter from the IRS?

Certified mail usually signals a deadline that protects your legal rights — like a Final Notice of Intent to Levy or a Notice of Deficiency. The IRS sends it certified so there's proof you were warned. These are time-sensitive: open it the same day and note the response date.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.