IRS Notices

Got a CP14 and Can't Pay? Your IRS Options in 2026

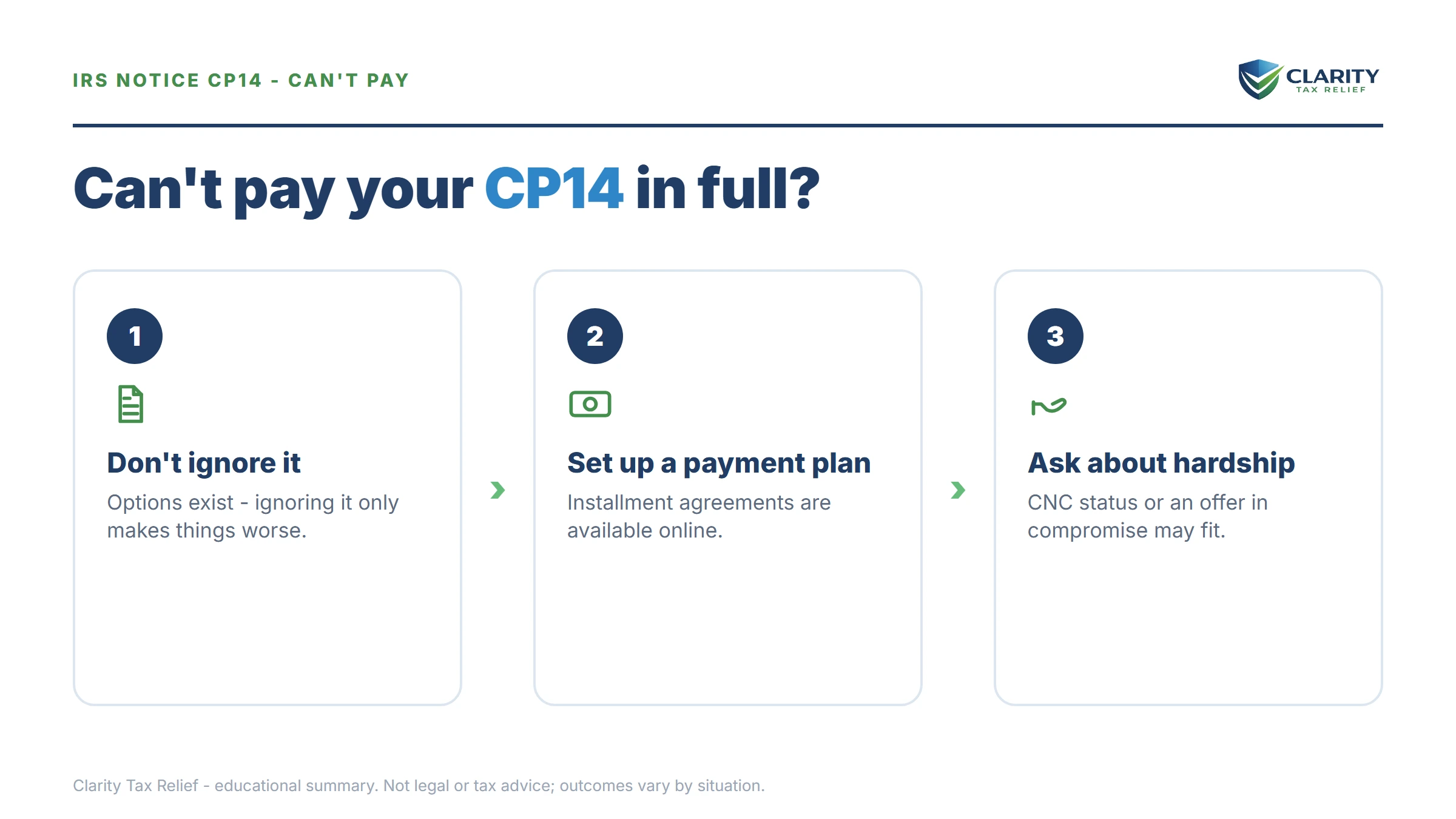

The short answer: if you got a CP14 and can't pay, don't panic and don't ignore it. The CP14 is just the IRS's first bill — no one is seizing anything yet. Before the deadline on the notice, set up a payment plan, request hardship status, or ask about penalty relief. Acting early is what protects you.

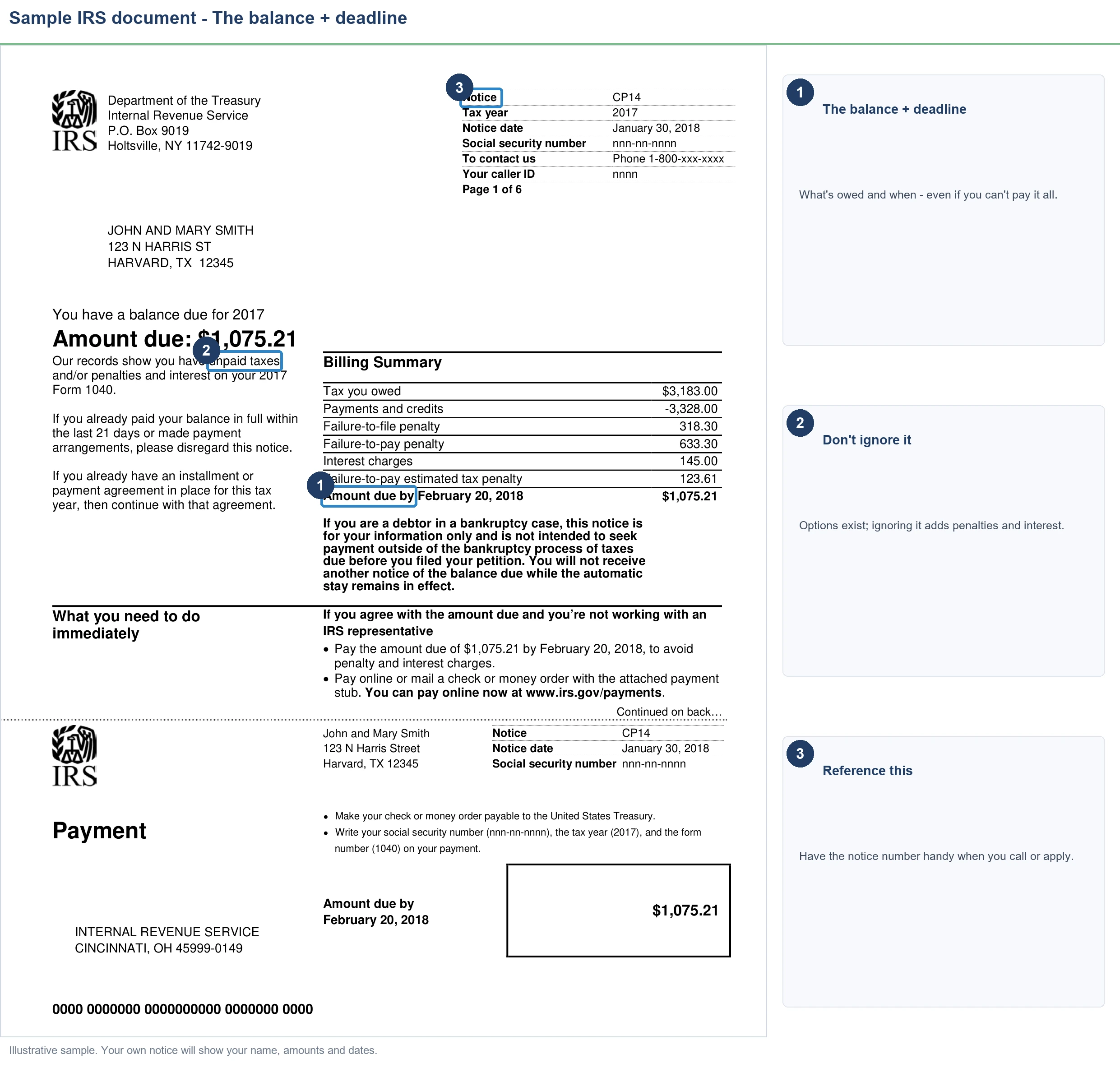

⏱ Your deadline: the "pay by" date printed on the notice — usually 21 days from the notice date (10 business days if you owe $100,000 or more). You don't have to pay by then — you just need to respond by then with a plan. Interest and a monthly late-payment penalty keep growing until the balance is cleared.

What a CP14 means when you can't pay it

A CP14 is the IRS saying its records show you owe money for a tax year — the amount, plus penalties and interest, is printed right on the notice. It's the first letter in the IRS collection sequence, not the last. If you got a CP14 and can't pay the full balance, that's a very common situation, and the IRS has built-in programs for exactly this. The notice just doesn't advertise them.

One thing to settle first: a CP14 is a bill, not an audit. No one is questioning your deductions. You can read the IRS's own explanation on the Understanding your CP14 notice page. For a full walkthrough of the notice itself, see our CP14 notice guide.

What happens if you ignore it

The hardest part of owing money you can't pay is the urge to set the letter aside. Don't. CP14s don't expire, and the sequence that follows is automated. Ignore each notice and the next one arrives roughly five weeks later — with more interest and more enforcement power:

- CP14 — first bill. You are here. No enforcement yet.

- CP501 / CP503 — reminder notices. Still just bills, but the balance keeps growing every month.

- CP504 — Notice of Intent to Levy. The IRS can seize your state tax refund, and a federal tax lien becomes a real possibility.

- LT11 / Letter 1058 — Final Notice. After 30 days, the IRS can garnish wages and levy bank accounts. You get formal appeal rights here — but far fewer good options than you have today.

Here's the encouraging part: simply responding to the CP14 — even just starting a payment plan — stops this whole chain in its tracks. The automated machine only escalates accounts that go quiet.

If you got a CP14 and can't pay: your real options

The notice makes it sound like there are two choices — pay in full or face consequences. In reality, the IRS has several programs, and which one fits depends on your finances:

- Short-term payment plan — up to 180 extra days to pay in full, with no setup fee. Best if you just need a little breathing room. Interest and penalties continue, but enforcement stops.

- Installment agreement — a monthly payment plan you can usually set up yourself. For balances under $50,000, "streamlined" agreements are approved without detailed financial disclosure, spread over up to 72 months. See the IRS payment plans page.

- Currently Not Collectible status — if paying anything would keep you from covering rent, food, and utilities, the IRS can pause collection entirely. The debt and interest remain, but garnishments and levies stop while you get back on your feet.

- Offer in Compromise — settling for less than the full balance. This is real, but only when your assets and income genuinely can't cover the debt. The IRS runs the math using strict formulas. An experienced tax professional can tell you whether you actually qualify before you spend anything chasing it.

- Penalty relief — if this is your first slip in years, first-time penalty abatement can erase the failure-to-pay penalty completely. Reasonable-cause relief may apply for illness, a disaster, or other events beyond your control.

A quick worked example. Say your CP14 shows $8,000. You set up a 36-month streamlined installment agreement. Once it's approved, the failure-to-pay penalty drops from 0.5% to 0.25% per month, the notice sequence stops, and you pay roughly $230 a month plus accruing interest — instead of waiting for a levy. The same $8,000 left ignored could be in CP504 territory within a few months.

Double-check the balance before you commit

A meaningful share of CP14s are wrong or already resolved. Before you set up a plan, spend ten minutes confirming the number is real:

- Log into your IRS online account and compare the balance there with the notice. Recent payments often cross in the mail with a CP14 — see our guide on getting a CP14 when you already paid.

- Match the notice against your return — same tax year, same amounts? If the figure looks off, read CP14 with the wrong amount before paying.

- Screen for scams: a real CP14 comes by postal mail, never email or text. Real payments go only to the United States Treasury or through IRS.gov — never gift cards, wire transfers, or payment apps.

How to respond, step by step

- Verify the balance against your IRS online account and your own records.

- Pay what you can now at IRS.gov/payments. Even a partial payment reduces the penalty and interest base going forward.

- Choose the option that fits — short-term plan, installment agreement, hardship status, or penalty relief — and set it up before the deadline on the notice.

- If the notice looks wrong, respond in writing with proof of payment or corrected figures, and keep copies of everything.

- If you owe more than $10,000, have unfiled years, or feel overwhelmed, get a professional review first. The order you fix things in — returns, then penalties, then the balance — changes what you ultimately pay.

Got a CP14 you can't pay right now?

Send us a photo of it. An experienced tax professional will tell you exactly which option fits your situation — and set up a plan that stops the clock. Free, confidential, no pressure.

CP14 "can't pay" questions, answered

What happens if I can't pay my CP14 at all?

You won't go to jail and nothing gets seized at this stage. Reach out to the IRS before the deadline and set up a payment plan or request a pause for hardship. The worst move is silence — ignoring the CP14 lets the automated notice sequence escalate toward liens and levies.

Can I set up a payment plan if I got a CP14 and can't pay?

Yes. Most people who owe under $50,000 can set up a streamlined installment agreement online in minutes, spread over up to 72 months, without detailed financial disclosure. If you just need a little time, a short-term plan gives you up to 180 extra days with no setup fee.

Will penalties keep growing if I'm on a payment plan?

Interest and the failure-to-pay penalty keep accruing until the balance is paid in full, but the penalty rate is cut in half — from 0.5% to 0.25% per month — once an installment agreement is approved. Setting up a plan also stops the notice sequence and any enforcement action.

What if I can't afford even a monthly payment?

Ask the IRS to place your account in Currently Not Collectible status. If paying anything would keep you from covering basic living expenses, the IRS can pause collection. The debt and interest remain, but garnishments and levies stop while your finances recover.

Can the IRS settle my CP14 for less than I owe?

Sometimes, through an Offer in Compromise — but only when your income and assets genuinely can't cover the debt. The IRS runs the math using strict formulas, not advertising slogans. An experienced tax professional can tell you whether you're actually a candidate before you spend time or money applying.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.