IRS Notices

Certified Letter From the IRS: What It Means and What to Do (2026)

The short answer: a certified letter from the IRS means the agency needs proof you received it — because it starts a legal deadline. These letters usually involve appeal rights, a proposed tax change, or a final warning before the IRS can levy. Find the notice number in the upper-right corner, then act before the date on the letter.

⏱ Your deadline: it depends on the letter, and certified ones are time-sensitive. A Final Notice of Intent to Levy (LT11 / Letter 1058) gives you 30 days to request a hearing. A Notice of Deficiency (CP3219 / Letter 3219) gives you 90 days to petition Tax Court. The clock starts on the notice date — not the day you open it.

Why the IRS sends a letter by certified mail

The IRS sends most of its mail first-class. When a letter arrives certified — the green slip, the signature line, the trip to the post office — it's because the law requires the IRS to prove you were notified. That proof matters because the letter triggers a deadline that affects your legal rights.

So a certified letter from the IRS isn't random. It almost always falls into one of three buckets: a collection action with appeal rights, a proposed change to your tax that you can dispute, or a request to verify your identity before a refund is released. The good news is that "certified" usually means you still have a window to respond — that's the whole point of the deadline.

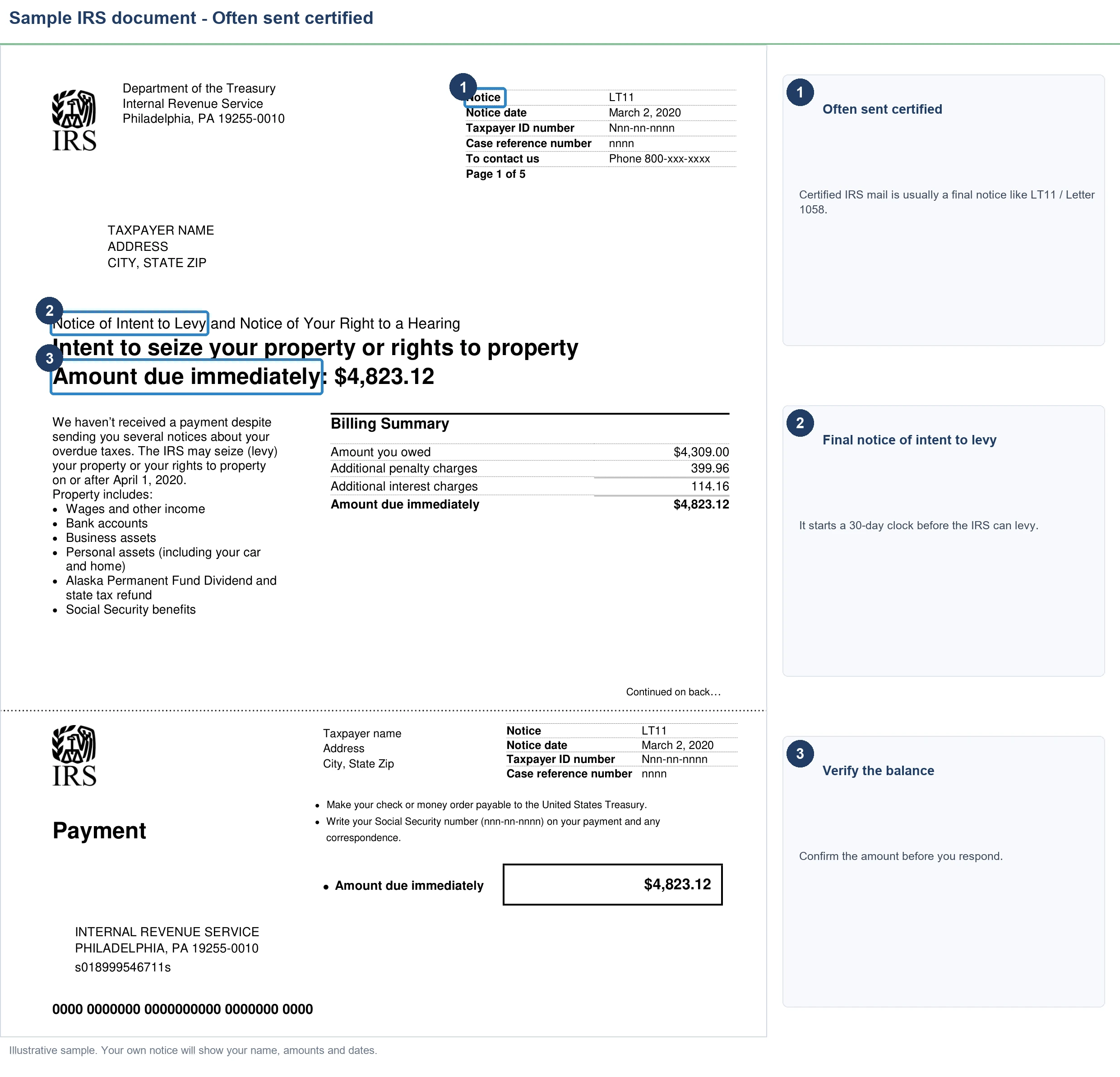

Decode it: what the notice number means

Look at the upper-right corner of the first page. That code tells you exactly what you're holding. Here are the certified letters people see most often:

- CP504 — Notice of Intent to Levy. A warning that the IRS can seize your state tax refund and is moving toward levy. Serious, but not yet the final step.

- LT11 / Letter 1058 — Final Notice of Intent to Levy and Notice of Your Right to a Hearing. The big one. After 30 days the IRS can garnish wages and levy bank accounts. You can file for a Collection Due Process hearing within those 30 days — see the IRS page on Letter 1058 / LT11.

- CP3219A / Letter 3219 — Statutory Notice of Deficiency. The IRS proposes additional tax. You have 90 days to petition the U.S. Tax Court (150 days if addressed outside the country). Details are on the IRS CP3219A notice page.

- Letter 3172 — Notice of Federal Tax Lien Filing. Tells you a lien has been filed and explains your appeal rights.

- Letter 5071C / 4883C — Identity verification. The IRS needs to confirm it's really you before processing a return or refund. Not a bill at all.

If your code isn't on this list, don't panic — the notice itself explains what it is and what to do. You can also look it up by searching "Understanding your [notice number] notice" on IRS.gov.

What happens if you ignore it

This is where certified mail bites. Because the deadline runs from the mailing date, refusing the letter or leaving it at the post office changes nothing — the clock keeps ticking. Here's what's at stake by letter type:

- Miss the 30-day window on an LT11/1058 and you lose your right to a Collection Due Process hearing. The IRS can then levy your bank account (banks hold levied funds for 21 days before sending them) or garnish your paycheck.

- Miss the 90-day window on a Notice of Deficiency and the proposed tax becomes final. You lose the chance to dispute it in Tax Court without first paying it.

- Ignore an identity-verification letter and your refund simply stalls until you respond.

In 2026, the IRS is short-staffed but its notices, liens, and levies are issued by automated systems. The machine doesn't wait for a human to review your file — which is exactly why the date on the letter matters more than how busy the IRS seems.

First: make sure it's real, and make sure it's right

Before you do anything else, take ten minutes to confirm two things:

- Is it genuine? A real IRS letter comes by postal mail, shows a notice number, and never demands gift cards, wire transfers, or payment by app. Payments go only to the United States Treasury or through IRS.gov/payments.

- Is the balance correct? Log into your IRS online account and compare what it shows against the letter. Payments and notices cross in the mail constantly, and some notices are simply wrong. If you got a separate bill first, our guide to the CP14 notice walks through verifying a balance step by step.

If the letter is incorrect, respond in writing with proof — don't pay something you don't owe assuming the IRS will catch its own error.

Your options once you know what it is

What you can do depends on the letter and your finances:

- Pay or set up a payment plan. If the balance is right and you can handle it, paying or starting an installment agreement stops the escalation. For balances under about $50,000, a streamlined plan over up to 72 months is often available without detailed financial disclosure.

- Request a hearing or appeal. On an LT11/1058, filing Form 12153 for a Collection Due Process hearing within 30 days pauses collection and gets a person involved.

- Petition Tax Court. On a Notice of Deficiency, filing within 90 days preserves your right to dispute the tax before paying it.

- Currently Not Collectible status. If paying anything would create real hardship, the IRS can pause collection. The debt stays, but levies stop.

- Offer in Compromise or penalty relief. Depending on your situation, you may qualify to settle for less than the full balance or to have penalties reduced — the IRS runs the math on eligibility. If you've already received a bill you can't pay, see what to do when you can't pay the IRS.

How to respond, step by step

- Find the notice number in the upper-right corner and match it to the list above so you know your exact deadline.

- Verify it's real and the balance is right using your IRS online account.

- Mark the deadline on your calendar — count from the date on the letter, not the day you opened it.

- Choose your path: pay, set up a plan, request a hearing, or dispute it with proof. Whatever you pick, start before the deadline — that alone stops most enforcement.

- If a levy, lien, or Tax Court deadline is involved, get a professional review fast. The order you handle things in — unfiled returns, penalties, then the balance — changes the outcome, and certified letters leave little room for do-overs.

Holding a certified IRS letter right now?

Send us a photo of it. An experienced tax professional will decode exactly which notice it is, how many days you have, and what your options are — free, confidential, no pressure.

Certified letter questions, answered

What does it mean when the IRS sends a certified letter?

It means the IRS needs proof you received it because the letter starts a legal deadline clock. Certified mail is usually reserved for notices with appeal or petition rights — like a Final Notice of Intent to Levy or a Statutory Notice of Deficiency. It's serious, but it almost always still leaves you time to act.

Do I have to sign for a certified letter from the IRS?

You don't have to sign, but refusing or ignoring it does not stop the deadline. By law the clock starts on the date the IRS mails the letter, not the date you open it. Signing for it simply means you'll know exactly what you're dealing with and how many days you have left to respond.

What happens if I don't pick up a certified letter from the IRS?

The deadline runs anyway. If it's a Final Notice of Intent to Levy, the IRS can begin garnishing wages or levying bank accounts 30 days after the notice date — even if the letter is still sitting at the post office. Ignoring it only costs you the time you'd have used to respond or appeal.

Is a certified letter from the IRS always bad news?

Not always, but it's never routine. The IRS uses certified mail for letters that carry legal rights and deadlines, so most are collection or audit-related. A few simply confirm something or ask you to verify your identity. Read it carefully — the notice number in the top corner tells you exactly what it is.

How do I know a certified IRS letter isn't a scam?

A real IRS letter arrives by postal mail, shows a notice or letter number in the upper right corner, and never demands payment by gift card, wire transfer, or payment app. Payments go only to the United States Treasury or through IRS.gov. You can verify any balance by logging into your account at IRS.gov before doing anything.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. If you're facing a deadline you can't meet, the Taxpayer Advocate Service is a free IRS resource.